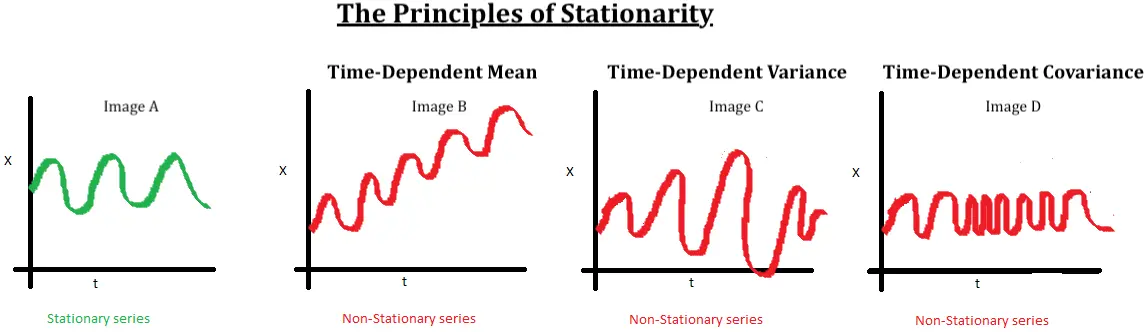

Definition

Let : Function of the lag and is independent of .

A stochastic process is weakly stationary

If it satisfies two conditions:

- (constant mean)

- (covariance independent of )

Weakly Stationary Process has Constant Variance

is weakly stationary, then is constant, independent of .

Relationship with Strict Stationarity

Relationship with Weak Stationarity

Let be strictly stationary process.

If is finite for all

The is also weakly stationary

Converse is Not True

Weak stationarity does NOT imply strict stationarity. A process can have constant mean and covariance without having identical distributions at different times.

Illustration